Refinance Break-Even Calculator Guide: When Does Refinancing Actually Make Sense?

Refinancing a mortgage sounds simple: get a lower rate, save money. But there's a catch. Every refinance costs money upfront-appraisal, origination fees, title work, recording, underwriting. Those closing costs can run $3,000 to $18,000, depending on your loan size. The question isn't "Is the rate lower?" It's "Are my monthly savings enough to justify the upfront costs-and do I stay in the home long enough to collect those savings?" That's where the break-even point comes in. It's a single number that decides whether refinancing makes sense or wastes your money.

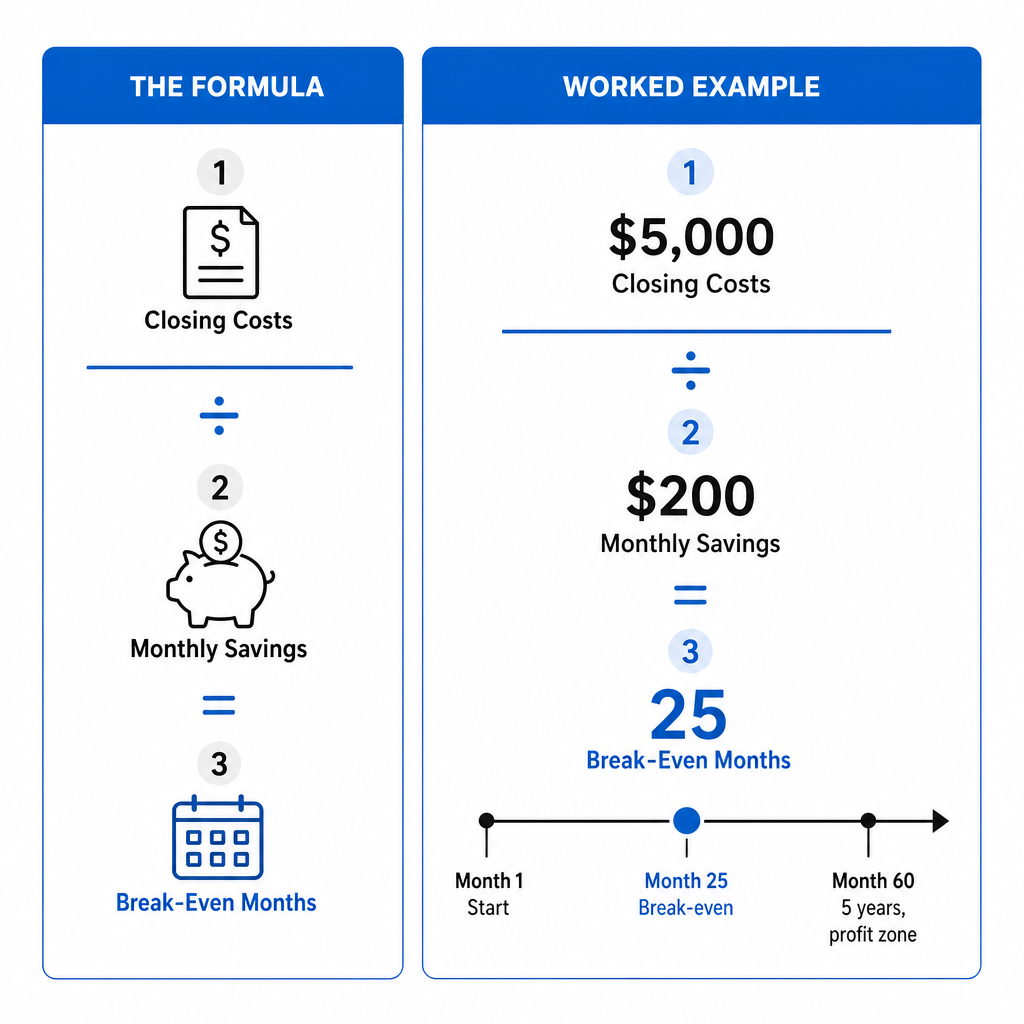

The Break-Even Formula

Break-even point (months) = Total closing costs ÷ Monthly payment savings. Divide your closing costs by how much your payment drops each month, and you get the number of months until refinancing "pays for itself."

The break-even formula: one line that matters

That's it. After the break-even point, every dollar of savings is profit. Before that point, the refinance is still recovering its upfront cost.

Worked example

- Your closing costs: $5,000

- Your monthly payment savings: $200

- Break-even: $5,000 ÷ $200 = 25 months (just over 2 years)

If you stay in the home for 5 years, you collect 3 extra years of savings-roughly $7,200 in profit. If you move in 1.5 years, refinancing costs you about $2,000.

Real homeowner scenarios: when break-even math wins or loses

Breaking the formula down is one thing. Seeing how it plays out in real decisions is another.

Scenario 1: Locked high in 2023, ready to move

A homeowner on Reddit locked in a 7.0% rate in 2023 on a $300,000 loan. Now in May 2026, they can refinance to 6.1%. Their current payment is roughly $1,996/month; the new payment would be around $1,847. That's $149/month in savings.

With typical closing costs of 3% (about $9,000), the break-even is: $9,000 ÷ $149 = 60 months (5 years).

The decision: If they're staying 7+ years, refinancing saves them real money-likely $10,000+. If they might move in 4 years, it's marginal. If they're job hunting and might leave in 2 years, skip it.

Scenario 2: Rate drop with short break-even

Refinancing from 6.875% to 5.75% on a $250,000 mortgage. The payment drops from $1,656 to $1,457-a $199/month win. Closing costs: $4,000 (negotiated).

Break-even: $4,000 ÷ $199 = 20 months (less than 2 years).

The decision: This is a strong candidate. Even if life throws curveballs and you move in 3-4 years, you still profit.

Scenario 3: The trap-dropping your rate but extending your loan

You've paid for 10 years on a 30-year mortgage. Your balance is now $250,000 on what started as a $400,000 loan. You can refinance to a lower rate-6.0%-but here's the catch: the new loan would also be 30 years, resetting your payoff clock.

Monthly payment looks great: it drops by $1,299. But you've extended your payoff from 20 years to 30 years. You'll pay significantly more in total interest, even though the monthly payment feels like a win.

The decision: Refinance to match your remaining term (a 20-year loan, in this case), not a 30-year. Your payment won't drop as much, but your total cost stays on track.

Scenario 4: PMI removal-a hidden game-changer

A first-time homebuyer put 10% down and has been paying PMI ($250/month) for 3 years. Home values appreciated; they now have 15% equity. They can refinance to conventional financing and eliminate PMI entirely-a $250/month savings.

Closing costs: $3,000.

Break-even: $3,000 ÷ $250 = 12 months.

The decision: This is a no-brainer. Even a modest home appreciation that triggered refinance qualification is a fast payoff. PMI removal alone often justifies a refinance, rate drop or not.

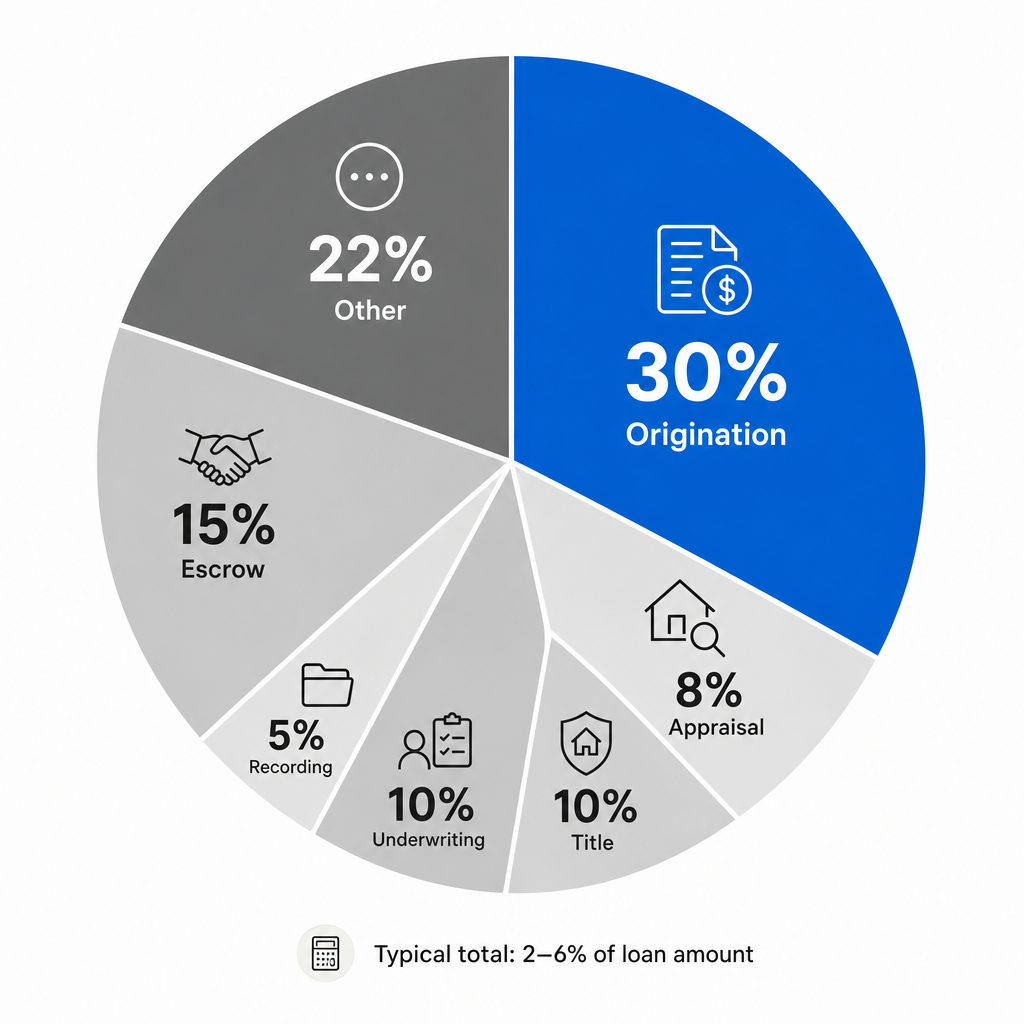

Closing costs: the upfront bill you can negotiate

Closing costs are the first barrier to refinancing. Typical range: 2-6% of the loan amount. On a $300,000 loan, that's $6,000-$18,000. But these costs are itemized-and many are negotiable.

What you'll pay

- Origination fee: 0.5-1% of loan (lender's cut)

- Appraisal: $300-$600

- Title search and insurance: $500-$1,000

- Recording and transfer taxes: $100-$500+ (varies by state)

- Underwriting and processing: $500-$1,000

- Escrow/closing agent: $500-$1,500

Ways to lower closing costs

- Shop lenders. Your first lender won't be your best. Get quotes from 3-5 lenders; fees vary significantly.

- Negotiate origination fees. Tell the lender you have competing offers. Many will waive or reduce this fee to win your business.

- Ask for lender credits. Some lenders will absorb fees in exchange for a slightly higher rate. Sometimes this trade-off makes sense.

- Request an appraisal waiver. If your home hasn't dropped in value, many lenders waive appraisals on refinances, saving $500+.

- Reissue your title policy. If you bought recently, your existing title insurance can be reissued at a discount.

- Check for employer programs. Some employers negotiate discounts with lenders; check with your HR department.

- Roll costs into the loan. A "no-out-of-pocket" refinance means you pay interest on closing costs, but you don't bring cash to closing. Calculate the 30-year impact first.

- Time your closing. Closing early in the month costs less in daily interest charges than closing near month-end.

Negotiating hard can save $2,000-$4,000, which dramatically shortens your break-even point.

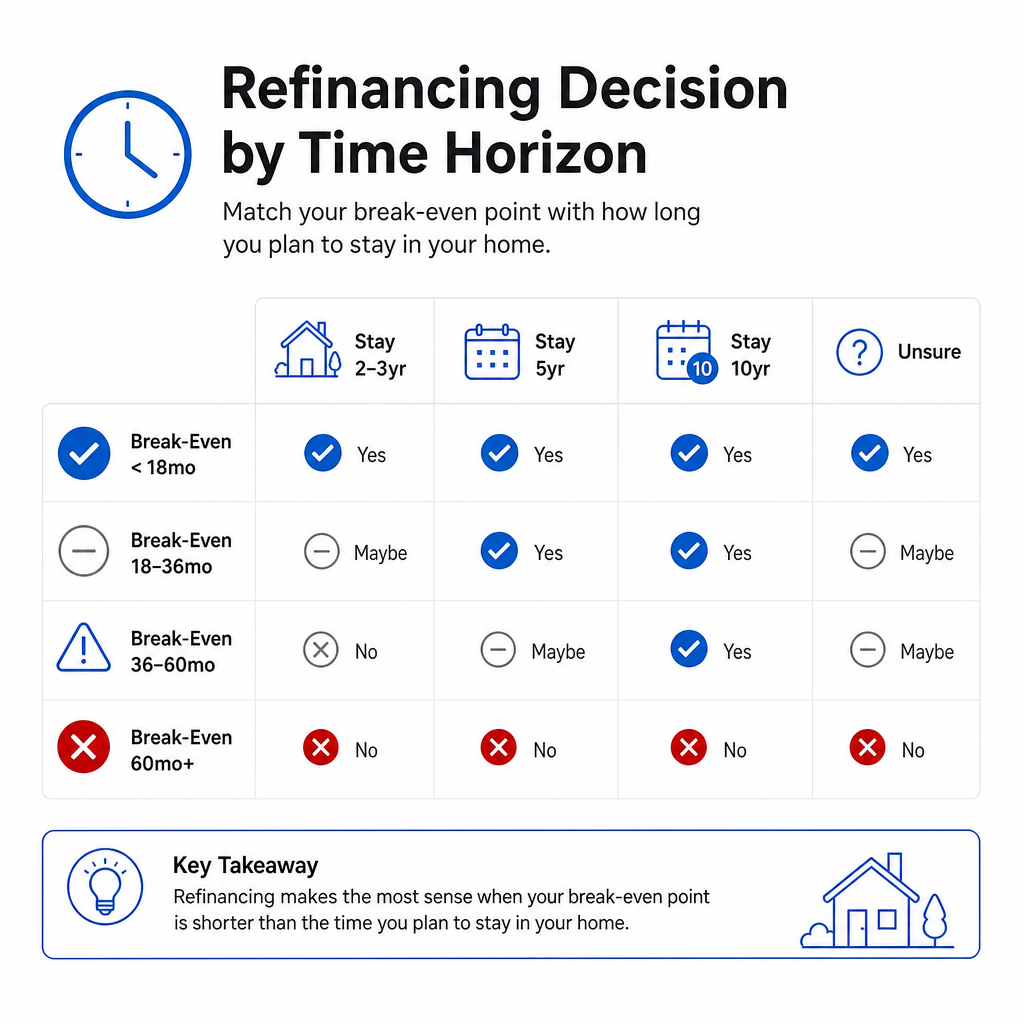

Time horizon: the real decision gate

The break-even formula is clean math. But the decision isn't mathematical-it's about your life. How long will you stay in the home?

- Staying 2-3 years: Break-even must be under 18 months. Any longer and you're gambling.

- Staying 5 years: Break-even up to 36 months is reasonable; you'll collect 2+ years of savings.

- Staying 10+ years: Break-even up to 60 months is acceptable; you'll collect 5+ years of savings.

- Unsure: Be conservative. If you can't confidently say you'll stay 5 years, make your break-even target under 24 months.

Life changes-jobs, family, health. Many homeowners thought they'd stay 10 years and moved in 4. Being conservative with your time horizon is usually smarter than gambling on a longer break-even point.

Cash-out refinance vs. HELOC: which tool for your goal?

If you need to access your home's equity-for renovations, debt payoff, or major expenses-refinancing isn't your only option. You can also use a HELOC (Home Equity Line of Credit).

Comparing your options

- Rate-and-term refinanceReplace your entire loan with better terms. Costs closing fees but locks in a fixed rate for 15 or 30 years.

- Cash-out refinanceTake out a larger loan and pocket the difference between old and new balance. Adds closing costs but gives immediate access to cash.

- HELOCA second line of credit secured by your home's equity, typically with lower fees and a variable rate.

When to use each

- HELOC wins if: You already have a low first-mortgage rate (under 5.5%) and want to avoid refinancing costs and rate resets. A HELOC preserves your existing rate.

- Cash-out refinance wins if: You need a large lump sum upfront AND you're okay with a higher overall loan balance and restarted amortization clock. Lock in a fixed rate for decades.

- Rate-and-term alone if: You just want to save on monthly payments without taking on new debt.

Use USFinNexus's refinance and HELOC calculators side-by-side to model each scenario and see which math wins for your situation.

The 2026 rate environment: where refinancing stands

30-year fixed rates are hovering around 6.36%, with 15-year rates at 5.71%. That's down from last year's peaks (6.81% / 5.92%), but still elevated compared to pandemic lows.

Forecasters expect rates to stay in the 6.0%-6.5% range through late 2026 into 2027. Translation: if your current rate is 7%+ (common for 2023-2024 borrowers), there's a refinance opportunity. If you're at 6.0%-6.25%, the potential savings are slimmer and break-even points stretch longer.

Don't wait for a perfect rate. The cost of waiting-staying at a higher rate for months-often exceeds the benefit of a slightly lower rate later.

Avoiding the big mistakes

Try USFinNexus

USFinNexus's refinance calculator does the break-even math for you instantly. Input your current loan, the new rate you're being offered, and your estimated closing costs. The calculator outputs your break-even date, monthly savings, and lifetime savings-all in seconds, with no email required and zero data collection.

No signup. No ads. No lender referral bias. Just the math. It works client-side (nothing leaves your browser), exports to a professional PDF in one click, and updates rates monthly from Freddie Mac's Primary Mortgage Market Survey.

Plug in your numbers and see if refinancing pencils out for your situation.